Erickson Financial Services, Inc. &

Emmett J. King, LLC

Colorado Health Insurance Broker & Group Benefits Adviser

Individual & Family Health Insurance in Colorado

What is Health Insurance and What Does Health Care Reform Mean for Me and My Family?

Health insurance is protection against the liability of medical costs. Effective January 1st, 2014, in compliance with the Patient Protection and Affordable Care Act (PPACA), everyone was required to obtain minimum essential coverage or incur a tax penalty. The penalty was called a "shared responsibility payment". Since the inception of the tax penalty, there has been much controversy over whether or not the tax penalty was Constitutional. Through executive order, President Trump has eliminated the "individual mandate" tax penalty effective January 1st, 2019.

What Qualifies as Minimum Essential Coverage?

An individual is considered to have minimum essential coverage for any month in which he or she is enrolled in one of the following types of coverage for at least one day.

- An employer-sponsored group health plan offered in a state, which is defined as the 50 states plus the District of Columbia. This includes plans offered by, or on behalf of, an employer to an employee, e.g. multiemployer plans, single employer collectively bargained plans, plans sponsored by third parties such as professional employer organizations, temporary staffing agency, etc.

- An individual health insurance policy offered in the individual market in a state or through an Exchange/Marketplace in a territory.

- A government plan such as Medicare, Medicaid, Children’s Health Insurance Program (CHIP), TRICARE (a U.S. Department of Defense Military Health System) or veterans coverage

- Insured student health coverage

- Self-insured student health coverage*

- Medicare Advantage plan

- State high risk pool coverage*

- Coverage for non-U.S. citizens provided by another country**

- Refugee medical assistance provided by the Administration for Children and Families

- Coverage for AmeriCorp volunteers**

*Designated as minimum essential coverage for plan/policy years beginning on or before December 31, 2014. For coverage beginning after December 31, 2014, sponsors of high risk pool or self-funded student health coverage may apply to be recognized as providing minimum essential coverage.

**Coverage provided by another country and coverage for AmeriCorps volunteers are no longer automatically deemed minimum essential coverage. However, individuals may apply to have their coverage recognized as minimum essential coverage.

How Can I Find an Affordable Health Insurance Plan for Myself and My Family?

Beginning October 1, 2013, the new "Marketplace", Connect for Health Colorado, will be open, and at this time, individuals and families will be able to shop for subsidized health insurance plans. If an individual does not want to shop for a subsidized plan (perhaps someone who does not qualify for a health insurance tax credit), he or she may also shop for health insurance plans outside of the "Marketplace".

Erickson Financial Services, Inc. is prepared to guide individuals and families through this process. We are fully certified to sell Colorado Health Insurance products both inside and outside of the "Marketplace", previously dubbed the "Exchange".

Does it Cost More if I Buy from an Agent or Broker?

Simply put, the answer to this question is, "No". Your final premium will be the same regardless of whether you buy from a broker, directly from the health insurance company, or directly from the new "Marketplace".

Health InsuranceTerminology

- In-Network vs. Out-of-Network - Before applying for health insurance coverage you will want to make sure that your favorite physicians and local facilities are in the network. Many of the new health insurance plans being offered through the new "Marketplace" will be HMOs, otherwise known as "skinny networks". These plans forbid you from seeking services from non-networked physicians, hospitals, out-patient facilities and labs. If you purchase a PPO plan, you may leave the network, but your out-of-pocket costs will be higher, so this is not recommended. In-network physicians, hospitals and pharmacies have contracts with the insurance companies they work with, and you cannot be "balanced billed" beyond the contracted rates. On the other hand, outside of the network, you can be billed if the cost of the service exceeds the "allowed" amount. Outside of the network, deductibles and copayments may be separate and higher than deductibles and copayments inside of the network. For the best coverage, always make sure that you use a participating provider. Your insurance company's website will always have a link to view participating doctors, hospitals and facilities online.

- Covered vs. Not Covered - "Covered" means the service is payable AFTER your deductible is met or it is payable AFTER a copayment is paid. A few services, such as preventive care (immunizations, paps, mammograms, prostate screenings, etc) must be covered at 100% with no cost sharing as a requirement of Federal Health Care Reform. Many people mistake deductible expenses as expenses that are not covered. For example, if your PPO plan's annual deductible has not been met yet, a trip to the lab for blood work might result in a deductible expense, an expense that reduces your calendar year deductible. In this case, you will be required to pay the network discounted fee for the blood test. This service is considered a covered expense, even though you have to pay for it. If the service is "not covered", it will not reduce your calendar year deductible.

- Deductibles - A deductible is the amount you have to pay out of your own pocket before health insurance benefits kick in for certain services. Most health care products and/or services are subject to a deductible, except preventive care and in many cases, routine sick visits and prescription drugs. Plan deductibles are almost always tracked by calendar year. If you purchase a policy late in the calendar year, your deductible will start over again in January. Some plans have a "per person" deductible, while other plans have a "family" deductible. Typically, insurance plans are less expensive when you choose a higher deductible plan. In terms of healthcare reform, Bronze Plans will have the highest deductibles and lowest premiums, while Silver, Gold and Platinum Plans will be more expensive and have lower out-of-pocket costs.

- Co-Insurance - Co-insurance is the percentage of healthcare costs that you will split with the insurance carrier after your calendar year deductible is met. Like the deductible, co-insurance is also typically tracked by calendar year and starts over again each calendar year. Typical Coinsurance splits are 80/20, 70/30, 60/40 and 50/50. You will continue to pay your portion of the co-insurance until your co-insurance maximum (out-of-pocket maximum) is met. The plan summary will always tell you what your co-insurance maximum is. Once the co-insurance maximum is met, your insurance carrier will pay 100% of covered expenses.

- Office Visit Co-Payments - An office visit copay is the flat dollar amount that you pay for a routine visit to either a primary care physician or a specialist, Coverage is 100% after the copay. Some catastrophic plans do not offer an office visit copay. Instead, the cost of a routine office visit can apply towards a plan deductible. Do not assume that your healthplan includes an office visit copay. Be sure to read your plan description to verify coverage for a routine office visit. When you pay a copay, your deductible IS NOT reduced by the amount of that copay, however, all plans now count copayments towards the plan's maximum out-of-pocket limit.

- Rate Changes - Insurance companies will typically renew your rates once per year. By federal law, insurance companies must spend 80% of your premiums on claims. The other 20% of your insurance premium may include administrative costs and profit. Typically, profit amounts to about 2-3% of your total insurance premium.

- Maternity Coverage - In Colorado, all insurance plans must cover maternity subject to the plan deductible and co-insurance.

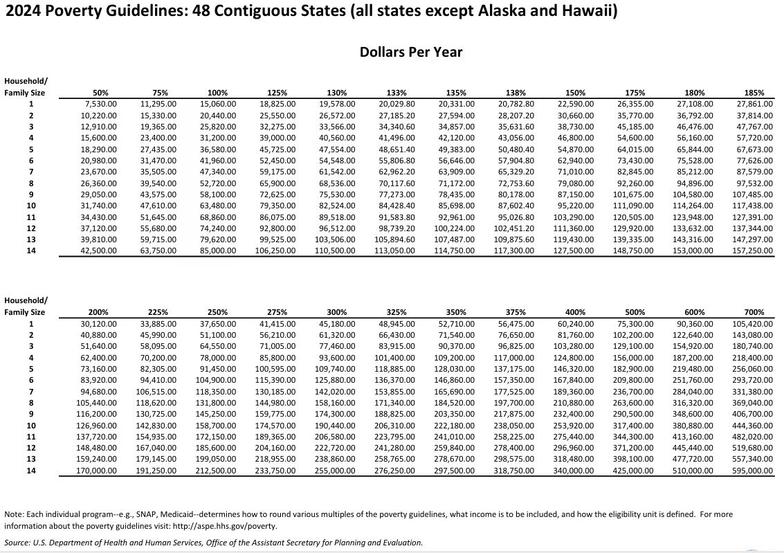

FPL Chart - 2024